A new era of investing.

What if I told you that you had an albatross hanging onto your investment account that was reducing your portfolio returns on an average of 2% per year?

And this albatross isn’t your investment management fees or expense ratios – it’s taxes.

Taxes are one of the biggest headwinds on an investment account, and according to an independent research study by Morningstar of pre- and after-tax investment returns from 1926-2023, they showed this was the average loss per year to a portfolio1.

So, the question is, what is there to do about it?

Why Mutual Funds and ETFs Limit Tax Efficiency

The first tip may be obvious to you – get out of mutual funds. Mutual funds are fantastic for quality diversification, but at the end of each year, you will receive your 1099 and have to pay capital gains tax on the performance of the fund.

Naturally, many people then turn to ETFs as an alternative—another strong option. However, like with mutual funds, you’re still capturing the performance of the entire fund. The key difference is that with an ETF, you only realize the gain when you sell your position.

So, regardless of a Mutual Fund or ETF/Index Fund, you are still in a pickle where you can’t control the tax implications of your investment very well.

And I am sure you have heard sentiment from your accountant or even your investment advisor, ‘if you’re paying taxes it means you made money’, and while that’s true, there is a more efficient way to grow your investments that will combat this drag on your portfolio and set you and your family up or significantly more wealth in the long term. Because who wouldn’t want to add 2% to their portfolio returns each year?

The answer lies within a strategy called direct indexing, and before I lose you on the technical terms of this industry, let me explain.

The Power of Direct Indexing in Wealth Management

Direct indexing is a strategy where, instead of investing in a fund that tracks an index, you own individual stocks that make up the index.

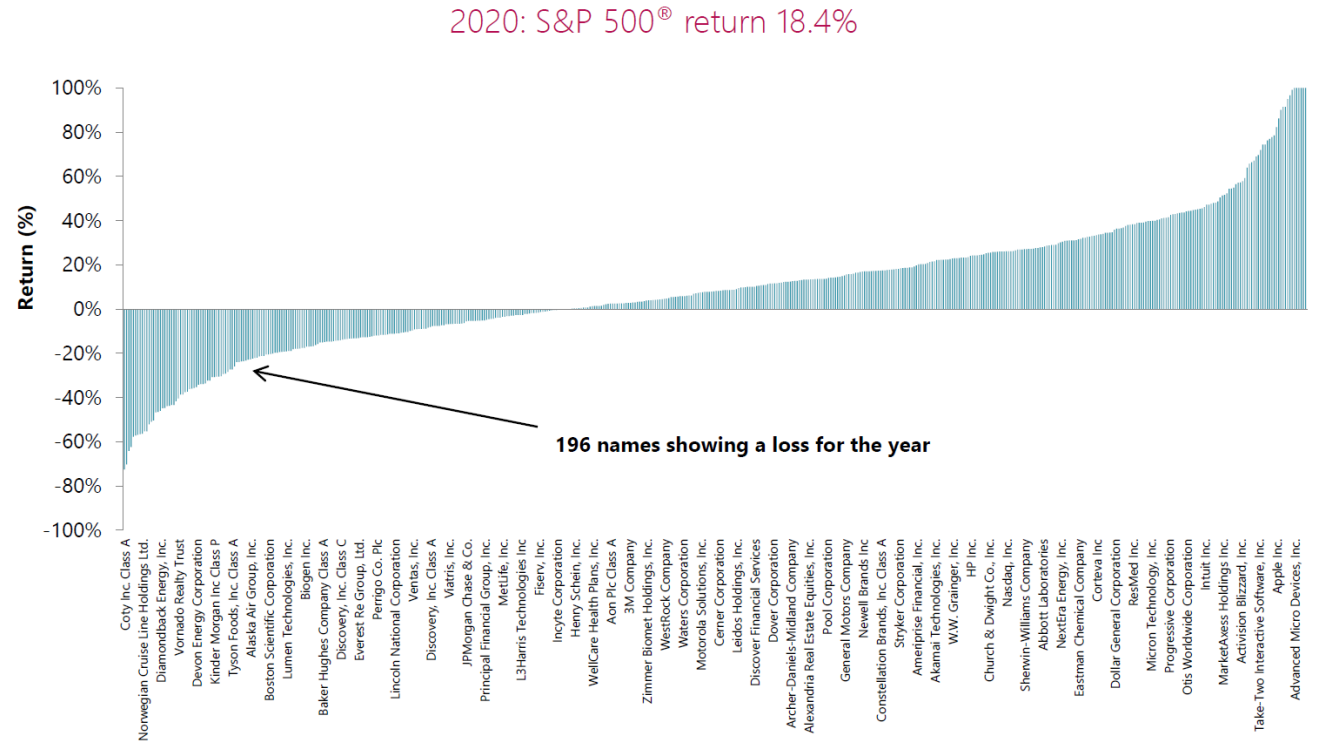

For example, in 2020, the S&P 500 had one of the best returns to date at 18.4% and if you were invested in the S&P 500 index, your return for the year would have been 18.4%.

Most investors would be thrilled with this. But if you look under the hood at how all 500 of these companies performed, not all were positive. Some companies absolutely crushed it, but 196 of them showed a loss for the year.

Had you instead owned the individual stocks in the S&P 500 rather than the index, then you would have been able to participate in tax-loss harvesting, aka selling the ‘losers’ to offset the ‘winners’.

How Tax-Loss Harvesting Boosts Portfolio Performance

When a stock declines in value, you can sell it to realize or book the loss. This is then used to offset the capital gains from your holdings that are performing very well, allowing you to raise the cost basis on the stocks that are appreciating – thus lowering your tax liability on your portfolio and effectively increasing your portfolio value.

The best part – due to how this strategy is managing stocks on an individual basis, you will see the benefits of this strategy in both a bull and bear markets through tax-efficient growth and tax-loss harvesting, respectively.

And while 2% may not sound mind-blowingly sexy, let’s say that you had a $2 million portfolio. 2% of that is $40,000 – now imagine adding that to your portfolio every year for 5, 10 or 20 years. And that $40,000 is continuing to compound and grow every year. That sounds pretty fantastic to us!

Achieve Smarter Wealth Preservation with Expert Guidance

At Nightingale Wealth Solutions, we specialize in tax-efficient wealth management strategies like direct indexing to help our clients reduce the tax liability of their estate and grow their wealth.

Our stock portfolios are held at a private trust company and have daily ongoing monitoring and adjustments by our investment team to optimize performance and tax efficiency. What makes strategies like this difficult, if not nearly impossible for an individual to implement on their own, is that it’s a full-time job to evaluate these companies every day to understand which ones should be held and which should be let go.

If you are looking for a way to drive down the tax headwind that is eating away at your performance and wealth, then direct indexing is a consideration that you can’t afford not to evaluate with the expert guidance of one of our advisors.

With a customized enhanced tax strategy and active portfolio management, you can achieve a more efficient use of your capital, preserve your wealth and scale this strategy as your portfolio grows.

Sources:

1Fidelity Investments. (2025, April 7). 3 reasons your portfolio may be underperforming. Fidelity Investments. https://www.fidelity.com/learning-center/wealth-managementinsights/3-reasons-your-portfolio-may-be-underperforming

2Custom Core Equity: Second Quarter 2021. (2021). Parametric. Slide 6.

Past performance is never indicative of future performance. This is not advice, but educational. Please consult a financial advisor before implementing any investment strategy to ensure it’s aligned with your financial plan. Tax loss harvesting only applies to non-qualified account registrations.

Securities and advisory services offered through Packerland Brokerage Services Inc., an unaffiliated entity – Member FINRA & SIPC.